What is Islamic Finance?

Islamic finance refers to financial services

and products that comply with the principles of Islam.

It involves activities such as savings, investing and financing

for sovereigns, corporates and retail customers.

These principles and the overall code of conduct in Islam

are part of what is known as “Shariah”;

which is adhered to by over 1.9 billion Muslims in the world.

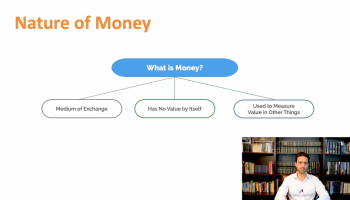

In Shariah, money is not a commodity and should only serve

as a medium of exchange to buy and sell goods and services.

This has an important impact not only on

how we think about banking and finance,

but also the way we do business with each other.

Since money is not a commodity,

then exchanging money for money with profit, in other words,

charging interest, is strictly prohibited and it is considered

in Islam a form of Riba.

Money must not be exchanged for money to make profit,

rather invested responsibly to create value

and support economic prosperity.

Islamic Finance stems from the values of Shariah,

which underpin a growing industry worth over $3 trillion,

with some of the largest financial institutions in the world

offering Shariah-compliant products.

Some of the core underpinning principles

of Islamic economics include:

Trusteeship:

In the Qur’an, humans are regarded as Allah's trustees on Earth.

Thus, humans have a duty to use the resources on earth responsibly

as they are trustees, not absolute owners.

Integrity:

Integrity is a core principle in Islam and governs all acts.

The Qur’an specifically directs the transacting parties

to deal with each other fairly and honestly.

Accountability:

Every person is accountable to God for their actions,

and as such, there is always ‘regulation’

of what a person does, in private or public.

If we harm another person unjustly,

this will be accounted for in the next life.

Piety:

Piety implies that people have to be devout both in private and in public

and that the values, norms and rules of Shariah

will be implemented in all circumstances.

The value of piety means that a person

should not be a means of harm to anyone, and neither should

their investments be directed towards harmful avenues.

As such, activities that cause harm to people and the environment

like alcohol, tobacco, and gambling

must be avoided in Islamic Finance.

Islamic Finance Products:

Islamic Finance operates both in the real economy

and financial economy.

In the real economy, real assets such as agriculture,

manufacturing, trade and other productive sectors are financed.

In the financial economy, many Islamic

securities are bought, sold and traded on the secondary markets.

Transactions in the financial economy

take place primarily in the Islamic capital markets.

Islamic finance products and services fall under either:

Islamic banking, Islamic capital markets

or Takaful (Islamic insurance).

Islamic financing takes place through asset-backed financing;

all forms of financing have an asset involved in the transaction

through either selling, investing,

leasing or developing an asset.

Financing is never done through cash for cash.

Some of the common financing contracts are:

Murabahah (Cost-plus Financing):

a sale of an asset with an agreed mark-up against an instant

or deferred payment.

Musharakah (Contractual Partnership):

a commercial enterprise

where all parties provide capital and share any profit and loss.

Mudarabah (Profit Sharing):

a contract between two or more parties where capital

is provided by one party

and the management and labour is carried about by the other partner.

Profit is shared between at an agreed profit share.

Ijarah (Leasing):

a contract which involves the leasing of an asset

for an agreed rental over a predetermined time period.

Islamic Finance has kept

pace with the rapid changes

in the market, adopting fintech and digital banking,

while companies and governments are increasingly issuing Sukuk

(Islamic financial bonds), namely green Sukuk.

Yet, while fintech is taking Islamic finance to the next level,

recent growth is still solidly based on

traditional banking services and products.

The Islamic finance industry was estimated

to be worth $2.8 trillion

and forecast to reach $3.5 trillion by 2024.

Malaysia, Bahrain and UAE remain

the top countries for Islamic Finance globally.

Another area of growth in Islamic Finance

is the increasing trend

and convergence with Sustainable Development Goals (SDGs),

ESG (Environment, Social and Governance),

ethical, and impact finance.

Shariah compliant products are screened

to avoid prohibited industries,

a practice that closely parallels ESG investing.

Like investors in Shariah compliant products,

investors using ESG screening strategies

avoid certain activities and products

so that their portfolios accord with the values of stakeholders,

align with the goal of developing a sustainable and fair society,

and do no harm to people or damage to the environment.

The values that Muslims express when they are investing

have significant overlap

with what is viewed as being ‘socially responsible’.

While there are some differences,

preserving the environment and social harmony

are at the heart of Islamic principles

in investing, financing, and conducting business.

Islamic Finance is still at a growing stage

and will evolve significantly in the coming years,

thanks to the advancement of fintech and the development of the SDGs,

ESG and socially responsible investing space.