Key Prohibitions in Islamic Finance

In this session, we will cover the key prohibitions in Islamic Finance.

We will define, explain and give examples of: Riba

Gharar,

Maysir,

and the prohibited activities

Riba:

Riba is sometimes translated as “usury,”

but in the modern context, usury refers

to an excessive rate of interest;

usury’s classical meaning refers to any rate of interest.

Linguistically, Riba refers to an unjustified increase or excess.

In Shariah terminology,

Riba refers to an unjustified and unwarranted charge

for the use of another’s money,

as well as unequal exchanges in homogenous items.

The scholars categorise Riba into two types:

Riba al-Fadhl:

the unequal exchange of Riba-based assets.

For example, exchanging 10 grams of gold for 12 grams of gold.

In a like manner, exchanging $1000 for $1200.

Riba al-Nasi’ah:

the delay in settling an exchange of two homogeneous assets.

For example, an interest contract where $1000

are exchanged with $1100 payable after one week.

Riba has been expressly prohibited in the Qur’an and Sunnah.

The Qur’an states: “Allah has allowed trade

and has forbidden Riba.” [Qur’an 2:275]

“O you who believe, do not consume Riba, doubled and redoubled.

Be mindful of God so that you may prosper.” [Qur’an 3:130]

The Prophet Muhammad (peace be upon him) said:

“(When) gold is exchanged in lieu of gold,

silver is exchanged for silver,

wheat is exchanged for wheat,

barley is exchanged for barley,

dates are exchanged for dates

and salt is exchanged for salt;

it must be exchanged in equal measure

and settled immediately;

and if the counter exchanges differ,

sell (whichever quantity) as you wish

as long as settlement is immediate.” [Sahih Muslim]

Riba in the modern day

The lending of fiat currency with interest is also a form of Riba

as declared in 1985

by the International Islamic Fiqh Academy of the OIC.

As mentioned earlier,

interest is absolutely prohibited in Islamic Finance.

Paying interest, receiving interest and facilitating interest

are all Shariah non-compliant activities and explicitly prohibited.

Interest is an injustice to the needy

and creates disparity between the rich and the poor.

But, if a bank cannot charge interest,

how do Islamic banks make profits?

Conventional banks use loan contracts,

hence, any premium on these loans is considered Riba.

However, Islamic banks use sale-based contracts for financing

and therefore can charge premiums on these transactions

because credit sale is permissible.

Application in modern Islamic finance:

Murabahah

Let’s take this example,

Jamal would like to purchase a US$20,000 car

and applies for Islamic financing with an Islamic Bank.

The Bank offers to finance his car using Murabahah.

The Bank buys this car from the dealer at US$20,000

on a cash basis then sells it back to Jamal

at US$20,000 (cost) + US$12,000 (profit)

on a deferred basis of 5 years.

In Murabahah financing,

both cost and profit should be disclosed to the client.

Jamal will pay monthly instalments for 5 years

until he settles the credit sale.

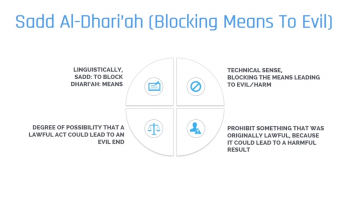

Gharar:

Linguistically, Gharar refers to ambiguity,

uncertainty and an unknown outcome.

Technically, Gharar refers to uncertainty

in the obligations and deliverables of a contract.

Gharar in the Qur’an and Sunnah

Although there is not an explicit mention of Gharar in the Qur’an,

the Qur’an prohibits all types of business transactions and contracts

which cause injustice

and inequality for any of the contracting parties.

Gharar results in inequality and an unlevel playing field

between the counterparties.

The Qur’an states:

“O you who believe,

do not devour each other’s property

by false means or unjustly,

unless it is trade conducted with your mutual consent.

Do not kill one another.

Indeed, Allah has been Very-Merciful to you.” [Qur’an 4:29]

Gharar includes uncertainty in:

the time of payment in a deferred sale,

the value of the subject matter,

the quality and the quantity of the subject matter,

ownership, deliverability,

availability, and the nature of the subject matter.

For example,

if the selling price, the item being sold

or the payment and delivery dates are ambiguous,

the transaction would have an element of Gharar

and thus be impermissible.

It is for this reason that sale transactions

that are contingent on an event

that is to occur in the future,

such as futures and forwards, are impermissible.

One of the reasons behind the prohibition of Gharar

is the tendency for such ambiguity to lead to dispute and discord.

Islamic finance seeks to preserve harmony in the society.

When transactions – day-to-day occurrences –

are filled with Gharar and ambiguity,

it can impact the very harmony of society.

Conventional insurance is prohibited because of the presence of Gharar.

The outcome of the exchange contract is uncertain and unknown,

potentially causing the policyholder to receive no benefit

despite paying premiums.

The Islamic alternative is what we call Takaful

which is an insurance where elements of Gharar

and Riba are not present.

Application in modern Islamic finance: Takaful

For example,

Ahmad subscribes to an education takaful plan with a Takaful Company.

Ahmad wants to make a hibah (gift)

of the takaful benefit to his child

to finance the cost of her education in the future.

If Ahmad dies before the maturity of the Takaful certificate,

all Takaful benefits will become the rights

of his nominated child

and will not be distributed amongst

the other legal heirs of the deceased.

However,

if Ahmad remains alive when the Takaful certificate matures,

the benefit will be surrendered to him.

Maysir: (Gambling or speculation)

Maysir is another core prohibition in Shariah.

Linguistically, Maysir refers to betting and chancing.

Technically, it refers to any activity where people stake

and bet their wealth on an unknown outcome,

whereby the winner wins all and the loser loses all.

Maysir applies to every activity in which

a person wins or loses his property by mere chance.

In common practice,

Maysir can refer to gambling, betting or speculation.

Maysir in the Qur’an

The Qur’an states: “O you who believe! Wine,

gambling, altars and divining arrows are filth, made up by Satan.

Therefore, refrain from it,

so that you may be successful.” [Qur’an 5: 90]

“Satan wishes only to plant enmity and malice

between you through wine and gambling,

and to prevent you from the remembrance of Allah

and from prayer. Would you, then, abstain?” [Qur’an 5: 91]

Contemporary examples of Maysir (gambling or speculation)

in finance are financial derivatives such as futures,

forwards, options and swaps.

In financial markets,

the end goal from trading these contracts

is to benefit from the price differences between sellers and buyers

by speculating on the price movement.

Generally, traders have no intention

of purchasing the underlying commodity.

Application in modern Islamic finance: Salam.

To understand more how Maysir element

can be avoided in any contract,

we can take the example of an instrument

in Islamic finance called Salam.

Salam is a forward transaction,

where the buyer can pay in advance for buying specified assets,

of which the seller will supply on a pre-agreed date.

What is given in exchange for the advance payment of the price

should not be in the form of money.

In other words, the object cannot be money.

For the payment in advance,

the contracting parties must stipulate

a future date for the supply of goods

of a specified quantity and quality.

To be valid, a Salam transaction needs to meet the following criteria:

The transaction is considered Salam

if the buyer has paid the purchase price

to the seller in full at the time of sale.

This is to provide a liquidity mechanism to the seller.

It is necessary that the quantity and quality

of the commodity are fully specified without ambiguity,

which may lead to a dispute.

All the possible details in this respect must be mentioned.

The commodity should be generally available in the market

at the time of delivery.

The time and place of delivery of the goods should be precisely fixed.

Although Shariah does not permit the sale of a commodity

which is not in the possession of the seller,

there is a consensus among Muslim jurists

on the permissibility of Salam.

Prohibited activities:

Moving on to the final main prohibition in Islamic Finance.

We have learned so far that

Riba (charging interest/usury), Gharar (ambiguity)

and Maysir (gambling or speculation) are forbidden.

This means that any company or industry

operating in line of these prohibitions

is considered as Shariah non-compliant.

For example, banks and all financial institutions

dealing in charging interest (Riba),

insurance companies because of the existing Gharar,

gaming industry because of the gambling involved

and financial trading because of speculation,

are Shariah non-compliant.

In addition to the prohibitions mentioned,

there are products and services

that are considered sinful in Islam

and therefore dealing in these products or services is not allowed.

For example, alcohol, tobacco,

pork, drugs and adult entertainment.

Hence sectors like hospitality,

alcoholic beverages, tobacco, pork

and adult entertainment are also Shariah non-compliant.

Application in modern Islamic finance:

Shariah stock screening

For investors who would like to grow their wealth

in a permissible way,

they cannot invest in companies

involved in any of the prohibited activities.

For this purpose,

the industry has developed Shariah screening

standards to select Shariah-compliant stocks.

Although the industry counts several Shariah screening standards,

the methodology is fundamentally the same.

It involves two layers of screening:

qualitative and quantitative screening.

Qualitative screening

Companies with more than 5%*

of their revenue coming from the following industries

are not allowed:

Alcohol Tobacco Pork-related products

Conventional financial services (such as banking, insurance, etc.)

Weapons and defense,

Entertainment

(such as hotels, casinos/gambling, cinema, pornography, music, etc.)

Quantitative screening

After removing companies with unacceptable

primary business activities,

the remaining stocks are evaluated according

to several financial ratio filters

to remove companies with unacceptable levels of debt

or impure interest income.

This screening considers the financials of companies

such as: Cash and interest-bearing receivables,

Interest-bearing debt,

and Impermissible income

Hence, only companies passing both screening stages

will be considered as Shariah compliant.

Module Summary

In this session:

We looked at the four key prohibitions in Islamic finance;

and Their applications in the modern Islamic finance.